From 6,000 BC to 21,000,000 BTC, Part II: The era of coins

In the first article of the Trezor series From 6,000BC to 21,000,000 BTC, we went through the ancient history of money. The part of history where our ancestors appreciated money because of its inherent value, not because of trust in the issuer of the currency.

Early ancient coins only rarely carried any face value, and their value was represented by the precious metals used to mint the coin. We discovered barter, commodity money, and even the first minted coins from the Kingdom of Lydia, 600BC; and that’s where Part II begins.

The era of coins

The Kingdom of Lydia’s days were numbered as the reign of Alyattes, one of its greatest kings and the creator of state-controlled coinage, ended. After Alyattes’ death, his son Croesus reigned over the kingdom from 560 BC to 546 BC and became the last king of Lydia.

Croesus was known for his wealth, and he’s credited as the issuer of the first pure gold coinage with a standardized purity (Croeseid). Croesus also implemented the bimetallic monetary system (bimetallism).

This was a crucial step in the development of modern monetary systems. For the first time in history, the monetary value of two precious metals had a set exchange rate; 1 golden Croeseid was equal to 10 silver Croeseids.

The ancient times

Shortly after Alyattes minted the first coin, the first Greek coinage (c. 600–550 BC) saw the light of day. This invention is generally attributed to Hermodike II, daughter of King Agamemnon of Cyme. It was essential to sustain the ever-growing demand for a payment method that could be easily carried by merchants and mercenaries.

Greek coinage introduced new minting standards and technologies, and drove the wide adoption of coins as a currency to over 1,000 Greek city-states. These city-states started minting their own coins and used them to pay for goods, taxes, and soldiers. These coins called drachma (pl. drachmae) were made of silver or gold and carried their natural value as precious metals in addition to their face value.

But it wasn’t just the Greeks who used state-minted coins as currency. Ancient Indians also started minting their own money around the same time period. The Great Kingdoms of India, known as Mahajanapadas, minted silver coins of standardized weight, but with irregular shapes and markings. Greeks created coins portraying city-state symbols such as the image of the Minotaur on coins from Knossos, or a symbol of a rose on Rhodes’ coins. Indian coins carried ancient symbols of power such as Dakshin Panchala coins with the swastika, or Saurashtra coins displaying a humped bull (zebu).

However, all of these coins had one major problem — the smallest coins of this period had a value of about one day’s salary, and that’s still too much to be used to buy a loaf of bread. These coins were simply too valuable to be used for everyday purchases. Imagine a world where the smallest denomination of currency is a coin worth $50. How are you going to pay for your $3 bread and ham if the merchant doesn’t have a coin that he can use to pay you back the remaining balance? This significant problem that had to be addressed to allow further economic and trading growth.

Everyday money for everyday people

It was once again the Greeks, known for their exceptional knowledge of mathematics, accounting, and economics who came up with new monetary standards addressing the issue of denomination.

Each of the three monetary standards of Ancient Greece — Attic, Athenian, and Corinthian — had different denominations of their drachmae, splitting them into smaller units called obol. These small fractions of silver minted during the Archaic period of Ancient Greece were ideal for everyday trading. They represented a lesser value, which allowed coins to be used for smaller everyday purchases, while silver drachmae were used for more significant exchanges such as the purchase of clothing, livestock, or tools.

The denomination of large, valuable coins into smaller obols made coins a crucial part of the lives of regular citizens. Thanks to denomination, money could be used by everyone who worked hard enough to earn it, and not just by the privileged elite.

Minting techniques went through further innovation during the Classical and Hellenistic period of Greece (480–31 BC), and some of the most valuable coins come from these two periods. Worth mentioning are the beautifully crafted Syracusan tetradrachma coins (c. 415–405 BC) depicting the head of the nymph Arethusa on the obverse and a racing quadriga chariot on the reverse.

During the Hellenistic period, the portraits of living people appeared on coins for the first time in Greek history. The largest gold coin, minted by Eucratides (171–154 BC), and the largest silver coin, minted by the Indo-Greek king Amyntas Nikator (c. 90–95 BC), also carried the portrait of their issuer.

Every new beginning comes from some other beginning’s end.

The Ancient Greeks and Romans were neighbors, enemies in battle, and regular trading partners. However, it took the Roman Republic a bit longer to invent coinage of the same quality and standards as the Greeks.

Romans used the aes rude trading system, which was based on a proto-currency in the form of bronze nuggets; it wasn’t until 326 BC that the first Roman coins made of bronze were minted. Shortly after, in c.211 BC, a whole new coinage system emerged in the Roman Republic. For the first time, Rome had its own principal currency — a silver coin called a Denarius (pl. denarii).

This revolutionary currency had several advantages compared to its predecessors. It was funded by a tax on property and war loot, and each Denarius represented the value of 10 bronze nuggets. Several other coins existed during these years, but the Denarius eventually became the primary currency and method of exchange across the early Roman Republic. For the first time in history, a coin currency was accepted across the whole territory, and the Denarius could be used as payment in all parts of the early republic.

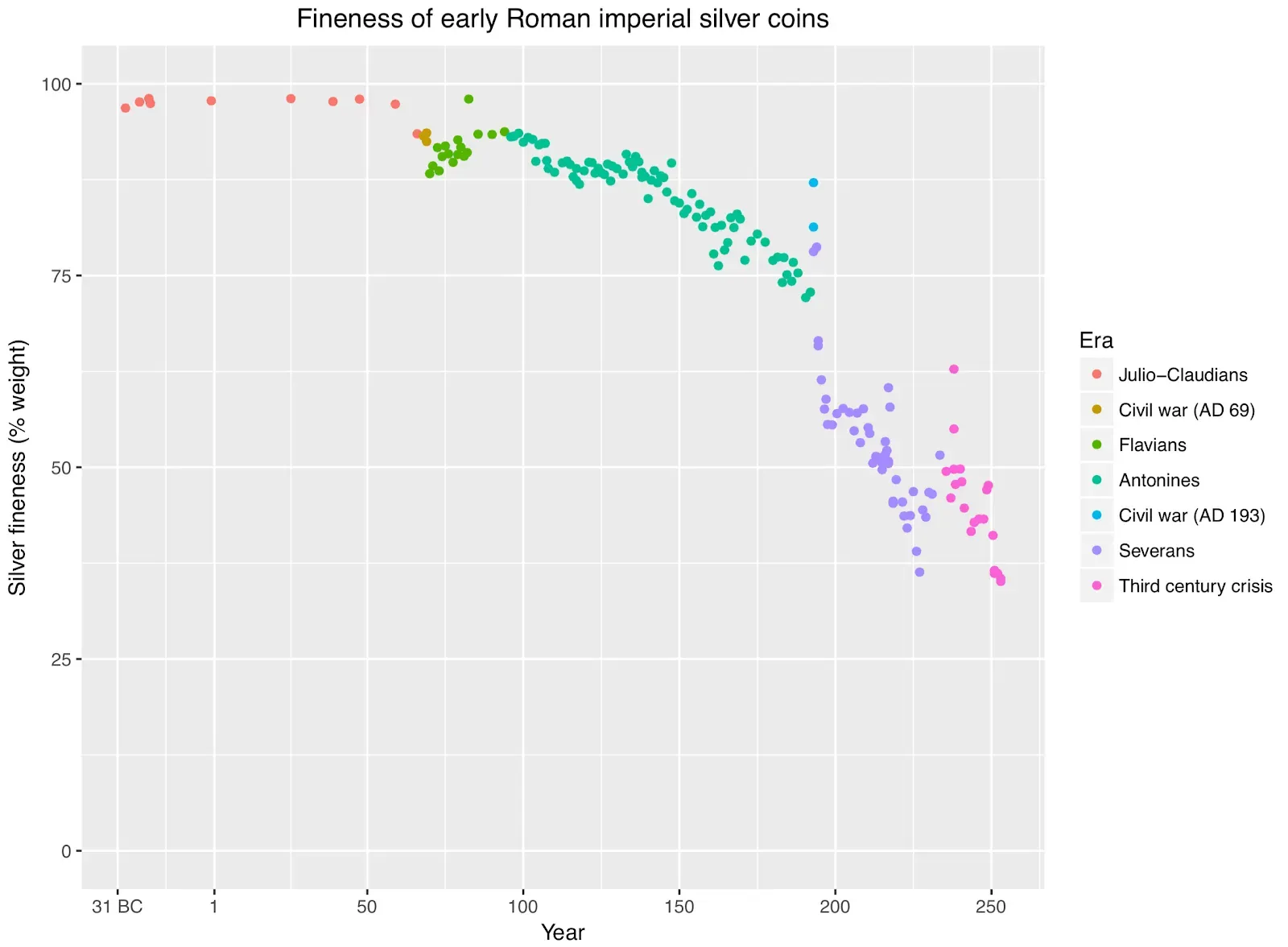

Unfortunately, it wasn’t all sunshine and rainbows for the Denarius, as it went through several cycles of debasement. This is a monetary practice of lowering the intrinsic value of commodity money, i.e., reduction in the quantity of silver used to mint denarii coins. These debasement cycles were mainly caused by the abundance of silver and gold generated from the ever-expanding Roman territory, but also by increased minting.

Both Sulla in 84 BC and later Julius Caesar in 46 BC increased the creation of new coins to fund the colossal Roman war machine. Debasement provided the Roman Republic with a short economic boost enabling the government to create more money to spend and pay debts. This resulted in inflation for Roman citizens, decreasing their purchasing power and wealth. A warning sign about the importance of sound money.

But Romans didn’t use Denarius just as a currency. Some of the most powerful and famous Roman emperors such as Julius Caesar, Marcus Brutus, or Augustus Caesar quickly discovered the additional potential of minting their own coins. In addition to being a medium of exchange and store of value, coins were also used as a propaganda tool. Caesar minted coins with his portrait to increase his popularity and allow regular citizens to see what their emperor looked like. In addition to his picture, Brutus minted the coins with two daggers on the reverse side.

“Brutus stamped upon the coins which were being minted his own likeness and a cap and two daggers, indicating by this and by the inscription that he and Cassius had liberated the fatherland.” — Dio (47.25.1)

The debasement of Roman coins didn’t stop with the end of the Roman Republic. In fact, it got even worse during the times of the Roman Empire. The debasement continued during the period of the Julio-Claudian dynasty when the first brass orichalcum sestertius coins were minted in Rome in 27 BC.

It’s unclear what exactly orichalcum was, but Cicero described it as a metal of gold color but much lower value. Orichalcum is believed to be an alloy consisting of copper, zinc, and other heavy metals. Rome moved from intrinsic money, known as sound or good money, to the coinage that was based purely on fiduciary value — bad money. The trend of minting coins built on their face value rather than the value of the used metals continued. In 64 AD, Nero even further reduced the weight and purity of precious metals used in Roman coinage.

This trend was followed by several emperors, and around 250 AD, the Denarius — made initially from pure silver — had now only a 25% silver content. The uncontrolled debasement, combined with other factors, pushed the Empire down to its knees, and in 235 AD the Crisis of the Third Century began.

Only after the crisis, Rome realized that a new set of rules has to be created to prevent such a disaster from occurring again. In 293 AD, the Roman emperor Diocletian, better known for separating Rome into the Western and Eastern Empire, reformed the Roman coinage system and set strict minting rules to prevent uncontrolled debasement.

Coins around the world As Rome struggled with its crisis mainly caused by the corruption and wrong decisions of the leading elites, the other great empires weren’t lagging behind.

The Sasanian Empire (224–651 AD), which was the last kingdom of the Persian Empire before the rise of Islam, had also developed its own coinage. Together with its sworn enemy, the Roman Empire, the Sassanids were the most influential money-issuing society of Late Antiquity.

Their main denomination was silver drachm, which was issued in smaller copper and silver fractions. Gold coins were minted only sporadically and mainly used for the purpose of publicity and to compete with Roman gold.

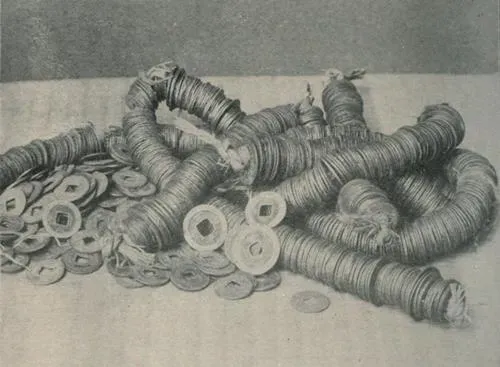

Further in the East, China split into the Three Kingdoms (220–280 AD) of Cao Wei, Shu Han, and Eastern Wu and minted its own coins. These coins, called cash coins, had a circular shape with a hole in the middle, and they were usually made of copper, which gave them a low value. This meant that the Chinese were able to make smaller, more precise payments compared to their distant relatives in Rome or Greece.

These cash coins had to be strung together on a string of cash to accommodate larger exchanges. The Chinese cash coins were so popular and practical that they didn’t go out of circulation until the late 20th century AD.

In the same period, the Indo-Scythian ruler of Western Kshatrapa, Rudrasimha I (178 to 197 AD), had also minted his own currency. Although not as aesthetic and of as high quality as the coins of Rome or Greece, these coins fulfilled their purpose nonetheless.

As the empires grew, and more and more people entered the market, the demand for coins also increased, and thousands of new coins had to be minted. All of the coins of this period were very similar and often represented around the same value, but all of them suffered from two flaws — denomination and centralization.

The increased demand for minting required coinage to become centralized and regulated. The government soon became the only authority with minting rights, and began to increase its minting capacity to pay debts and purchase goods. The government quickly realized it could create more coins by reducing the purity and content of the precious metals used.

The monetary policies of this period were still evolving, and the rulers weren’t too bothered about breaking these policies for their personal benefit. The coins of early antiquity were ripe with inflation and denomination and set a precedent for the creation of fiat currencies. Currencies with no intrinsic value, based on trust in the issuer.

The counterfeit history

If you think that counterfeiting is somehow a new technology, you would be wrong. Counterfeits are as old as money itself, and counterfeiting was often called “the world’s second-oldest profession.”

The first counterfeit money appeared at the same time as the first coins of Lydia. The creation of fake coins took several forms, such as mixing precious metals with base metals, or shaving the coin edges and using the shavings to mint additional coins.

Counterfeiting wasn’t as frequent in history as it is in the present, but records of counterfeit coins indicate that it was an issue of every historic monetary system. The early German and Slavic tribes were regularly attempting to counterfeit Roman coinage, which forced the Roman Empire to establish a new profession of testers.

Testers were responsible for the verification of coins in circulation and were often punished with lashes if they failed to recognize a counterfeit coin. If a merchant was found using counterfeit currency, all of his goods were seized, and he was punished with lashes.

And what about paper?

Although paper was invented in 100 BC by Chinese scholars, it took another two hundred years to develop an affordable method of paper manufacturing. In 105 AD, during the Han Dynasty, a government official named Ts’ai Lun was the first to start a paper-making industry.

At that time, paper was only used to record important information, and it wasn’t widely available to the public. Paper didn’t take the form of money until the rule of the Tang Dynasty (618–907 AD), but that’s for another part…

End of part II.